This project is a collaboration between EBAC and Banco Original, a Brazilian financial institution that operates in retail, corporate, open banking, and rural segments. In 2013, Banco Original pioneered fully digital banking in Brazil, becoming the first to allow 100% online checking account openings.

Problem Statement

Credit restriction is a widespread issue affecting millions of Brazilians. Many loan applications are denied or granted with lower-than-expected values. Most users do not understand the underlying reasons for rejection, such as low credit scores or financial restrictions associated with their CPF (Cadastro de Pessoas Físicas).

Key questions:

• How can we help users better understand their credit profile?

• How can users improve their financial health and credit scores?

• How can we assist users with financial restrictions in organizing their finances?

Research & Insights

Current Financial Landscape in Brazil

• 46 million unbanked individuals: In 2019, one in three Brazilians over 16 years old did not have a bank account, despite moving R$1 billion through informal transactions.

• 63.2 million Brazilians in debt: This represents 40.4% of the adult population. The average debt per person is R$3,258.69.

• Financial literacy gap: Only 21% of Brazilians received financial education before the age of 12, and 37% do not discuss finances with their partners.

Pandemic Impact on Financial Behavior

The COVID-19 pandemic amplified financial difficulties. We analyzed how Brazilians interacted with digital credit solutions during this period, identifying pain points such as lack of reliable financial information, unclear lending processes, and security concerns regarding personal data.

User Research & Methodology

To create a user-centered solution, we employed:

• "How Might We?" Framework: To identify opportunities for improving user financial literacy and credit access.

• CSD Matrix (Certainty, Assumption, Doubt): To validate research hypotheses.

• Stakeholder Mapping: To align product decisions with business needs and user expectations.

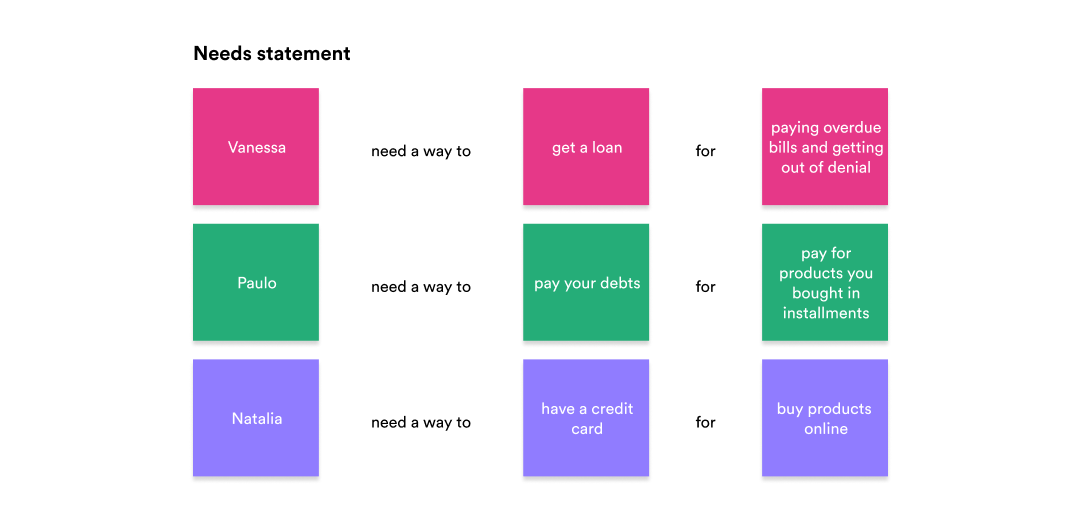

• User Interviews & Proto-Personas: We categorized users into four groups: Battler, Autonomous, Connected, and Conscious. Interviews provided insights into motivations, needs, and behaviors.

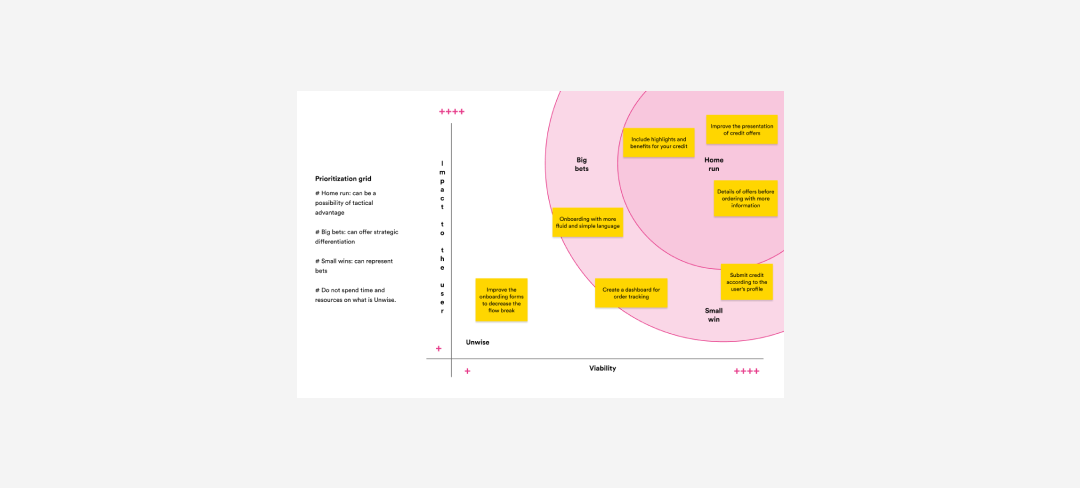

• Empathy Mapping & Prioritization Grid: To define the most impactful and feasible features for development.

Preserved data to maintain respondents' privacy.

Preserved data to maintain respondents' privacy.

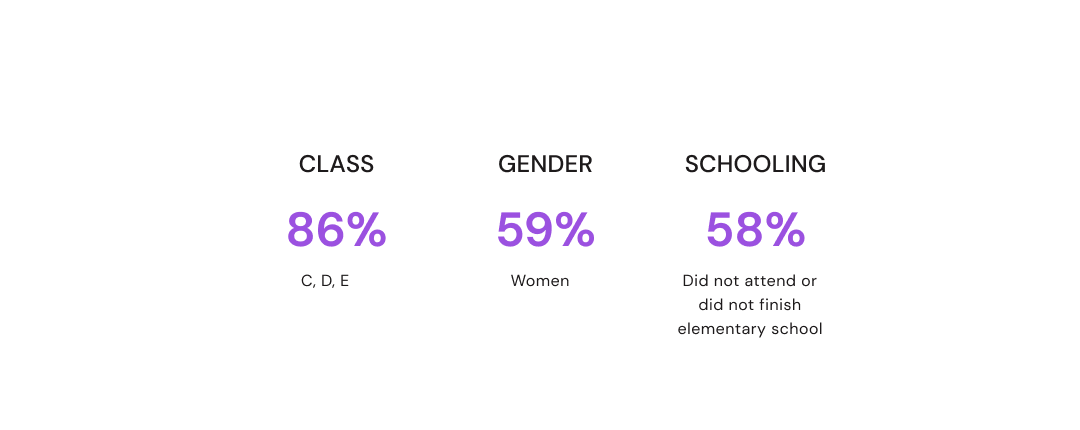

Key Findings

Positive Behaviors:

42% of the target audience is young, and 84% already used banking apps before the pandemic.

Users actively seek financial education and credit simulation tools.

Negative Behaviors:

Fear of sharing confidential financial data.

Difficulty understanding loan terms and credit score impact.

Young users applying for credit cards out of necessity, without financial literacy.

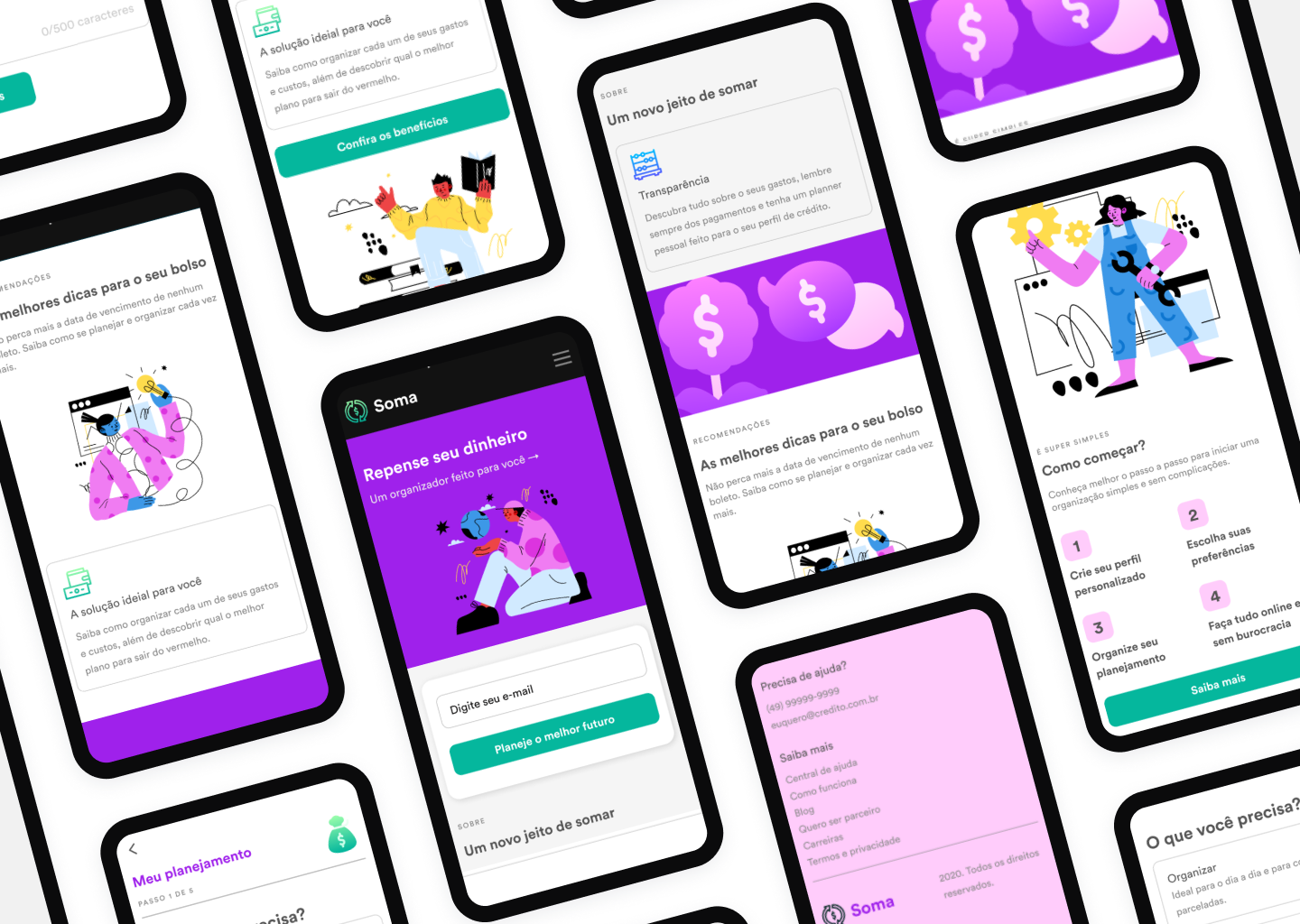

Solution: Soma - A Digital Financial Assistant

Concept: Soma is a digital platform designed to help users improve their credit scores, manage finances, and make informed financial decisions. The platform offers:

• Personalized credit profile analysis.

• Financial education content tailored to different user needs.

• An expense organizer to track spending and improve creditworthiness.

• A digital wallet for better financial management.

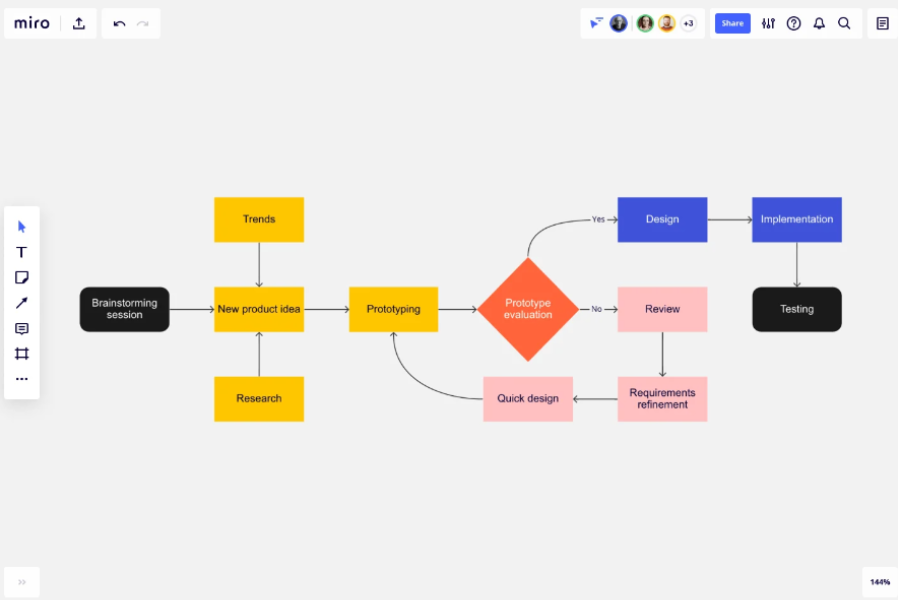

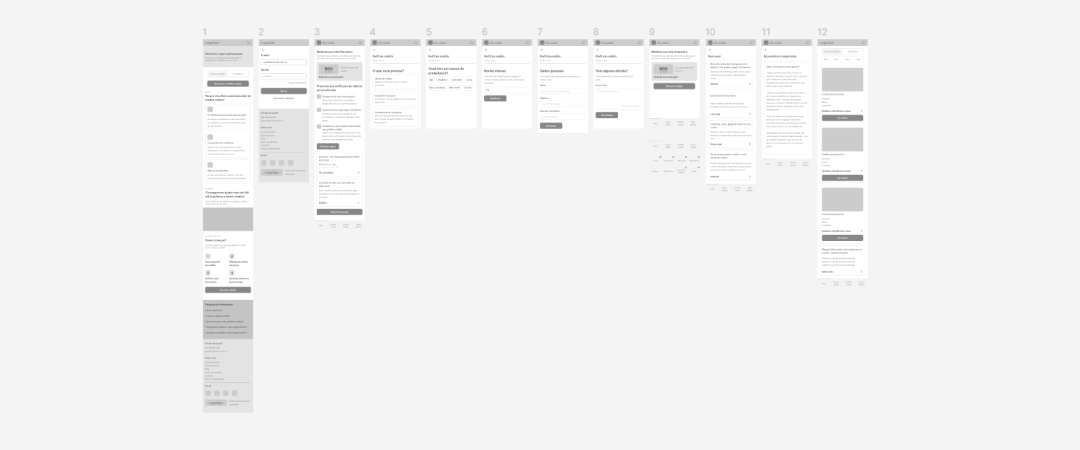

UX/UI Design Process

Usability & Prototyping

• Designed an intuitive interface focused on clarity and accessibility.

• Simplified the credit application process to reduce friction.

• Developed a personalized dashboard displaying real-time credit score updates and actionable insights.

• Integrated financial education modules with interactive tools.

Iterative Design & Testing

• Conducted usability testing with real users, gathering feedback to refine navigation and features.

• Prioritized enhancements based on user feedback, emphasizing simplicity and transparency.

Impact & Business Feasibility

User Benefits:

Improved understanding of financial health and credit scores.

Increased access to fair credit opportunities.

Enhanced financial planning capabilities.

Business Benefits:

Strengthened Banco Original’s positioning as an advocate for financial education.

Increased user engagement through personalized financial tools.

Potential for revenue generation through premium financial advisory services.

Learnings & Next Steps

• Conduct usability testing with a larger sample size to refine user experience.

• Enhance security features to address concerns about data privacy.

• Expand financial literacy offerings with interactive learning experiences.

Final Thoughts: Soma bridges the gap between financial literacy and accessibility, offering a user-friendly platform that empowers Brazilians to take control of their financial future. By prioritizing usability, transparency, and personalized financial guidance, this solution aligns with Nielsen Norman Group’s best practices in UX/UI design.